3.2.4.1 Progressive and Regressive Taxation

(This is an archived page, from the Patterns of Power Edition 3 book. Current versions are at book contents).

Some taxes are designed to be levied at a higher percentage upon those who have greater wealth in that category: they are ‘progressive’. The justification for such a policy is discussed later in this chapter, as an extension to 'economic reciprocity' (3.5.1.2).

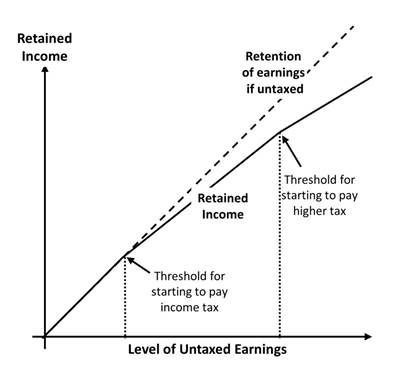

Income taxes, for example, tend to be progressive. They typically take the form of allowing all income below a certain threshold to be free of tax and then taxing the remainder. Usually a higher tax rate is applied as incomes exceed a further threshold, on the principle that the rich can afford to pay even more – as in the simplified example illustrated below, which rises from 0% to 20% to 40%.

The American and British income tax schedules are progressive,[1] as are those in

most other countries.

Some other taxes are progressive, affecting the wealthy more than the poor, such as taxes on land value,[2] property, inheritance and capital gains. Thomas Piketty has suggested that a “progressive global tax on capital” could be levied.[3]

In contrast, the American Social Security Fact Sheet in 2017 revealed that it was ‘regressive’: only applying to incomes up to $127,200. Purchase taxes (including value-added tax) also tend to be regressive on many commodities, because poorer people spend a higher proportion of their incomes on basic requirements.

Tax is directly proportional to income in a ’flat tax’ system: it is neither progressive nor regressive. Its proponents, some of whom are libertarians, argue that it stimulates growth by avoiding ‘penalising’ high earners. It also avoids the distortions of special allowances and is cheaper to collect.[4]